Solar PV is a crucial pillar of clean energy transitions worldwide, underpinning efforts to reach international energy and climate goals. Over the last decade, the amount of solar PV deployed around the world has increased massively while its costs have declined drastically. Putting the world on a path to reaching net zero emissions requires solar PV to expand globally on an even greater scale, raising concerns about security of manufacturing supply for achieving such rapid growth rates – but also offering new opportunities for diversification.

Solar PV Manufacturing today

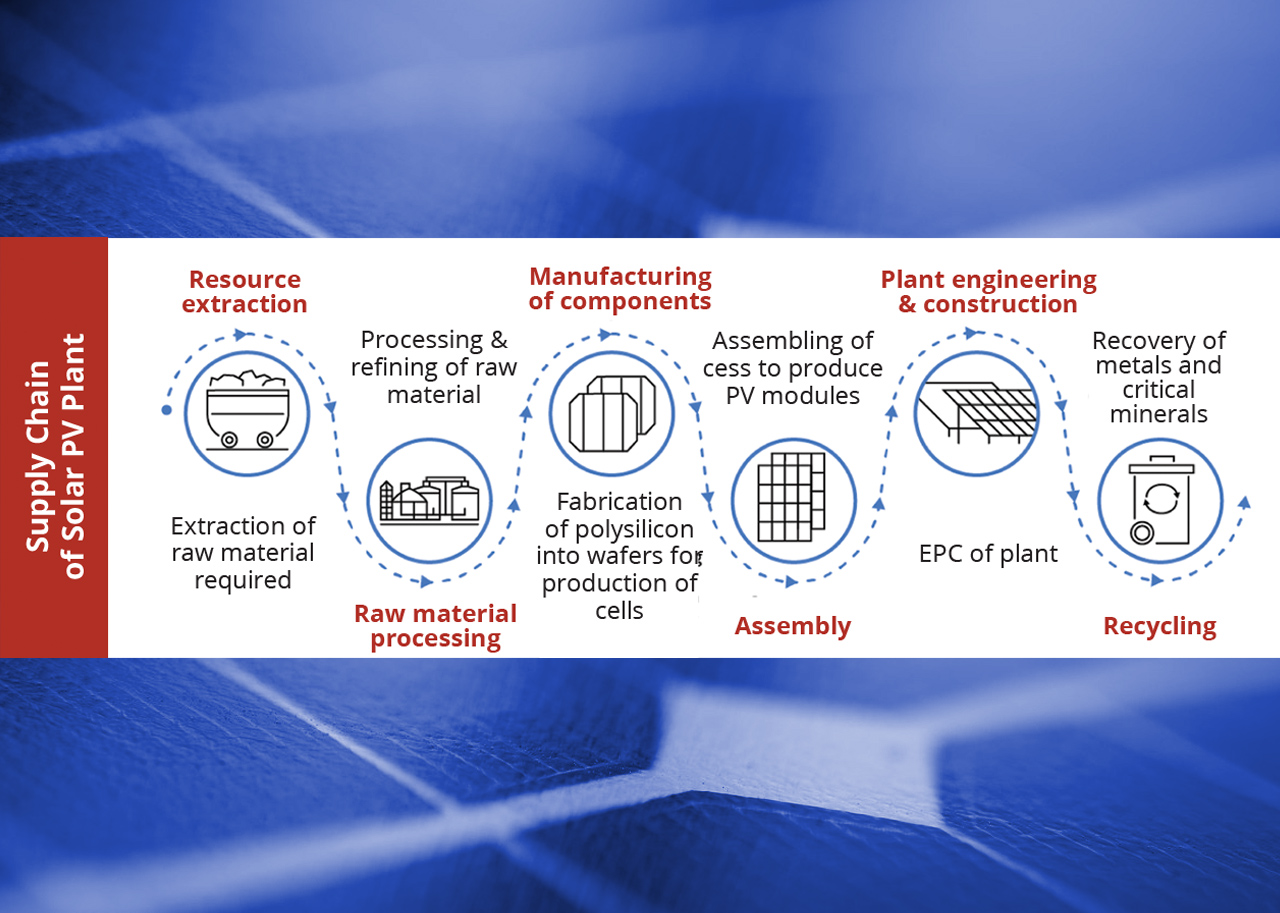

The Current Status of Global PV Supply Chain

A major geographical shift has occurred in solar PV manufacturing capacity and production over the last decade. China has strengthened its leading position as a manufacturer of wafers, cells and modules between 2010 and 2021, while its share of global polysilicon production capacity almost tripled. Today, the country’s share in all manufacturing stages exceeds 80%, more than double its 36% share in global PV deployment.

For wafers, China has very little competition, while for cells and modules Southeast Asia has considerable manufacturing capacity, mostly in Viet Nam, Malaysia and Thailand. For polysilicon, Germany continues to be a major supplier for the c-Si PV modules industry, while the United States and Japan possess significant capacity but focus their production on semiconductor-grade products. Considering manufacturing plants under construction and planned, China’s dominance in solar PV manufacturing is expected to persist or even expand in the short term.

Although countries in North America and Europe have significant module-manufacturing capability, they depend almost entirely on China and Southeast Asia for solar cells, except for manufacturing capacity linked to thin-film technology, which relies less on the Chinese supply chain. In addition, China is also the main manufacturer of module components including glass, EVA, backsheet and junction box.

Low solar cell prices, the possibility of sourcing several panel components locally (frame, glass, wiring and packaging), trade restrictions and government support have encouraged many companies around the world to invest in module assembly lines. Accordingly, 38 countries had module assembly capabilities in 2021, by far the highest of all steps of the PV manufacturing process. In many cases, however, investments were relatively small or stopped at the pilot stage, with just 19 countries having assembly capacity of at least 1 GW.

Companies in several countries and regions are contemplating significant expansions to their manufacturing capacity in upcoming years, notably in India, Viet Nam, Thailand, the United States and the European Union. However, with over 300 GW of new assembly plants under consideration in China, its market share is expected to remain high in the medium term. Given ongoing and planned investments in manufacturing capacity, in addition to innovation and further potential for efficiency gains, crystalline silicon technology is expected to dominate the solar PV market for many years to come.

Taking together polysilicon, wafers, cells and modules, the total value of PV-related trade reached USD 40 billion in 2021 – an increase of over 70% from 2020. International solar PV trade volumes depend strongly on China’s domestic demand because the country is both the largest producer and consumer of polysilicon, wafers, cells and modules. Furthermore, in the last five years it has been the main importer of PV-grade polysilicon, mainly from Germany, Malaysia and Japan, as its domestic production has fallen short of local demand for wafer production.

In 2017-2021, Southeast Asian module manufacturers were responsible for onethird of global PV module exports, directed mostly towards the United States and the European Union, where Chinese modules were subject to various trade restrictions. The rest of the market was dominated by China, with its shares in India and Brazil exceeding 90%.

When it comes to PV equipment manufacturing, the market have changed dramatically over the past decade, with leadership shifting from Europe, the United States and Japan to China. Driven by the exponential expansion of global demand, the total number of firms entering the PV equipment manufacturing market surged 150% during 2007-2020 to almost 1 900, with the number of Chinese firms almost quadrupling during this period to more than 700 (RTS, 2021). Today, all top ten equipment manufacturers are in China and claim over 45% of the global market share.

Solar PV supply chain vulnerabilities:

Concentration along the PV supply chain at the jurisdictional, geographical, plant and company level make the supply chain vulnerable to single incidents, whether they be a country’s individual policy choices, a natural disaster, a war, a pandemic, technical failures or individual company decisions. Historically, all these risks have materialised, leading to higher prices and likely slowing the pace of solar PV deployment.

For instance, a 2020 explosion at a polysilicon facility in China put 8% of global polysilicon production capacity out of operation. This is the largest of four polysilicon plant closures in 2020 resulting from flooding and technical issues. While each incident occurred at a different time, together they led to an estimated 4% decline in annual production in an already-tight polysilicon market, contributing to the near tripling of prices between 2020 and 2021. In 2021, silicon and wafer production in China were also curtailed when regulators required producers to cut production as part of energy-saving measures. As of early July 2022, a fire at polysilicon facility in Xinjiang and the ensuing maintenance requirements reduced global production by 0.5%. Even this comparatively small disruption contributed to price increases.

Concentrating production within a single geographical region or country also exposes the supply chain to risks from changes in diplomatic relations among countries as well as alterations in domestic policies and infrastructure. For instance, shipping times from China to US and European ports increased from around 40 days to more than 100 following the Covid-19 outbreak. Overall, polysilicon, wafer, cell and module production capacities are all becoming more concentrated, leaving the supply chain more vulnerable to risks.

The production capacity of solar PV supply chain segments is also concentrated at the company level, introducing vulnerabilities to another set of risks. Concentrating production capacity among just a few companies introduces the risk of having a small set of companies working together to increase profits at the cost of higher consumer prices and quicker dissemination. This situation can lead to collusion, price fixing, dumping and other behaviours that reduce competition and ultimately boost prices and retard deployment.

Wafer production capacity is considered moderately concentrated. Polysilicon market shares are more distributed among the top five companies, so production is less at risk of competitiveness impacts than that of wafers. Meanwhile, cell and module manufacturing capacity is more distributed than that of polysilicon and wafers, implying fewer competitiveness risks.

High company concentration in the solar PV supply chain makes the financial health of large companies key to the sector’s long-term sustainability, especially considering the formidable investments and expansions needed by 2030.

Poorly designed and implemented trade policies, and uncertainty around them, can lead to price increases, delayed investment and slow solar PV deployment. As trade is critical to provide the diverse materials needed to make solar panels and deliver them to final markets, supply chains are vulnerable to trade policy risks.

Supply Chain Diversification: Challenges & Opportunities

Supply chain disruptions during the Covid-19 crisis, record raw material prices and the Russian Federation’s (hereafter, “Russia”) invasion of Ukraine have raised numerous questions concerning the high dependency of many countries on imports of energy, raw materials and manufacturing goods that are key to their supply security. The solar PV supply chain is one of the most geographically concentrated supply chains globally, as China dominates raw material mining and refining and manufactures over 90% of critical inputs such as polysilicon, ingots and wafers. Key countries and regions with ambitious decarbonisation targets (including the United States, Europe and India) are therefore considering or already implementing policies to attract investment to localise manufacturing in multiple solar PV supply chain segments.

Diversification of the solar PV supply chain has both costs and economic benefits countries need to assess when designing and implementing policies. To assess these, countries should consider multiple factors such as job creation, investment requirements, electricity prices, CO2 emissions, manufacturing costs and, finally, recycling.

CO2 Emissin & Electricity Prices: A more geographically diversified solar PV supply chain could offer opportunities to reduce manufacturing emissions if new facilities are built in places with access to electricity that is less carbon-intensive than where current production is. At present, manufacturing modules generates far more emissions than transporting them to demand centres does. In fact, the single largest source of solar PV industry emissions is indirect emissions from electricity consumed in manufacturing. In 2021, the electricity used to produce solar panels was responsible for 89% of PV industry emissions globally, compared with just over 8% from direct consumption of fossil fuels and over 3% from transport. Thus, ambitious electricity decarbonisation goals in many countries will help reduce overall global solar PV manufacturing emissions.

However, domestic solar PV manufacturing is not always less carbon-intensive than importing from China. For example, at today’s power mixes, producing the entire supply chain in India or Australia would generate more manufacturing emissions than importing the finished modules from China. India’s solar PV ambitions for both demand and supply, supported by concrete policies, are critical for solar PV supply chain diversification and resiliency. In the short term, however, manufacturing the entire solar PV supply chain in India would be almost 15% more emissions-intensive than in China. Therefore, a compromise between total or partial self-sufficiency and lower emissions will need to be reached while high-emissions-intensity countries work towards decarbonising their domestic power generation.

Among all supply chain segments, the largest scope for reducing manufacturing emissions intensity through diversification is in polysilicon and wafers. However, maintaining competitiveness in these segments will also require that manufacturers have access to electricity at costs comparable with or lower than today’s global averages. For instance, the average price of industrial electricity is close to USD 90/MWh for polysilicon and wafer production. In India, new polysilicon or wafer production may be more economically challenging than in other countries in the region due to higher industrial electricity prices (USD 100/MWh). While industrial electricity prices in China are in the range of USD 60-80/MWh excluding subsidies, which enables cost-competitive manufacturing in many provinces.

Investment Cost: High investment costs for polysilicon and wafer manufacturing challenge the business case for projects outside of China.

The amount of initial capital needed to establish a solar PV manufacturing facility varies significantly by country/region, type of equipment used, and costs associated with land, construction and financing. A manufacturing facility’s size has a direct impact on the economies of scale that can be realised, affecting investment per megawatt. According to recently commissioned plant and equipment price data, polysilicon plants and ingot and wafer factories are significantly more CAPEX-heavy than cell- and module-manufacturing facilities. In addition, because of the considerable infrastructure investments needed (USD 200-400 million), Greenfield polysilicon plants are not usually bankable for capacities of less than 10 000 Mt (around 3 GW).

For polysilicon, ingot and wafer manufacturing, benefitting from economies of scale is crucial to realise lower per-megawatt investment costs. Recent Greenfield polysilicon plants in China range in size from 40 000 Mt to 100 000 Mt, almost tripling historical averages.

Investment costs in the United States, the European Union and India are three to four times higher per megawatt than in China and ASEAN countries for polysilicon, ingot and wafer production. Longer construction and development timelines, considerable labour and material costs, the higher cost of capital, a lack of economies of scale and a dearth of knowhow in developing mega-scale PV manufacturing facilities remain key reasons for higher costs. For instance, experience in developing large-scale ingot and wafer manufacturing facilities is very limited outside of China, as the country holds over 95% of the market share.

Manufacturing Cost: Manufacturing cost parity across regions and countries is critical for solar PV supply chain diversification. While cost differentials dictate whether a country’s solar PV products are cost-competitive, they are also critical for policymakers to design policies that effectively support the solar PV sector, including manufacturing plants. Solar PV production costs currently vary widely across both components and locations.

Based on modelled assumptions for each supply chain segment, the total cost of producing modules in key countries and regions varies from USD 0.24/W in China to USD 0.33/W in Europe, excluding profit margins, taxes and transport fees.

Relatively low energy and investment costs (which lead to lower depreciation costs) and inexpensive labour make China the most cost-competitive location to manufacture all components of the solar PV supply chain.

Large variations in energy, labour and depreciation inputs (due to relatively high investment costs) make PV manufacturing 9% costlier in India and around 20-35% more expensive in the United States, Europe and Korea.

Thus, diversifying solar PV manufacturing will depend on the ability of nascent and new markets to match the cost efficiencies evident in China. For instance, realising economies of scale and integrating plants and processes can reduce variable costs to increase competitivity.

Job Creation: Job creation is one of the main arguments for expanding domestic manufacturing of any product, as many governments consider manufacturing jobs to be sustainable. Thus, given solar PV’s critical role in the energy transition and its job creation potential, it is a key industry for the global expansion of manufacturing jobs.

For policymakers, the job intensity of various solar PV supply chain segments can be an important factor, especially when designing incentives to support the manufacturing sector. For instance, according to estimate that producing 1 GW of c-Si solar module capacity per year could create as many as 1 300 full-time manufacturing jobs, covering polysilicon, ingots, wafers, cells, modules and other materials such as glass, backsheet and EVA. The most job-intensive segments along the PV supply chain are module production (requiring 600-900 jobs) and cell manufacturing (450-650 jobs).

PV manufacturing requires a diversity of workers, including production engineers, material handlers and assemblers. Due to the current geographical concentration of the solar PV supply chain, the majority of skilled personnel is based in China and Southeast Asia, so diversification will require a concerted effort to train new employees. Thus, any strategy to increase PV manufacturing capacity must include a workforce training component. While governments and employers have already introduced training programmes for new employees, training must be co-ordinated and scaled up to provide the amount of labour needed to secure investment in local manufacturing facilities. There is not currently enough trained labour for PV manufacturing, especially in small or emerging manufacturing markets, given the low amount of job opportunities available.

Recycling: Solar PV modules currently have an estimated average service lifetime of 25-30 years, after which time their performance can deteriorate and they can be subject to failures. Considering historical capacity additions, we estimate that the global cumulative flow of decommissioned solar PV capacity will reach around 7 GW by 2030 and could increase to over 200 GW by 2040. This represents 400-600 kt of embodied materials cumulatively by 2030 and 11-15 Mt by 2040. As setting up effective policy frameworks and value chains can take time, it is crucial that governments, industries and other stakeholders prepare now to manage the future surge of solar PV waste from a systemic, circular-economy perspective.

Managing end-of-life (EoL) flows of solar PV equipment is an environmental challenge. In addition to contradicting circularity principles, putting PV panels in landfills can cause environmental pollution and health issues due to the presence of hazardous materials such as lead. In this context, the benefits of recycling are manifold: it provides not only an alternative to land filling, but also the pportunity to recover valuable elements and secure a reliable secondary source of raw materials for the PV industry and other sectors.

Furthermore, because it provides a domestic supply alternative, recycling can alleviate energy security concerns for countries heavily dependent on imports. It also helps avoid negative environmental, social and health impacts associated with raw-material mining, and can reduce the energy and environmental footprint of solar PV. Moreover, reconditioning and recycling can generate employment opportunities and support local economic activity.

Last but not least, in addition to recycling, circular approaches aimed at improving solar PV designs for reuse, enhancing product longevity and developing remanufacturing will be pivotal to diversify the solar PV supply chain and shrink its environmental footprint.

Conclusion:

A country’s policy and macroeconomic environment is critical to attract investment in manufacturing facilities for any industry. For solar PV, governments worldwide have implemented multiple policies and incentive schemes, with varying success. In simple terms, solar PV manufacturing policies can provide direct support to manufacturing investors, or they can indirectly stimulate investments by creating an attractive investment environment. Support policies can be applied on the supply side (upstream) or the demand side (downstream), through four possible combinations described below.

Direct:

Supply:

- Manufacturing tax credits for one or multiple solar PV supply chain segment manufacturing facilities.

- Grants for one or multiple solar PV supply chain segment manufacturing facilities, including to cover land and infrastructure costs.

- Low-cost financing for greenfield solar PV manufacturing facilities, or for their expansion or operation.

- Lower energy prices for energy-intensive PV manufacturing facilities.

- Lower income tax rates for solar PV manufacturing companies.

- Lower import tariffs and VAT rates for imported manufacturing equipment.

- Government funds to reduce labour costs through lower charges.

- Incentives for to exported goods manufactured domestically.

Demand

- Local-content requirements for domestically manufactured equipment attached to policies to stimulate solar PV demand.

- Solar PV power plant auctions/tenders linked to commissioning new manufacturing facilities.

Indirect:

Supply:

- Import tariffs or trade duties to raise the cost of imported solar PV equipment and related products.

- Import bans on solar PV products not meeting certain sustainability standards or regulations, to set standards for imported PV equipment.

- Border CO2 tax adjustment for imported solar PV products.

- Carbon footprint standard for modules in tenders.

- R&D and innovation funds, or funds for academics and the private sector to develop solar PV technologies.

- Tax incentives to employ highly skilled labour for R&D.

- National or sub-national funds to educate skilled labour for solar PV manufacturing.

- Government investment to upgrade infrastructure, including for logistics, waste management and power, including industrial clusters.

Demand:

- Policies to stimulate domestic solar PV demand (tax credits, FITs, auctions).

- Local-content premiums for domestically manufactured equipment attached to policies to stimulate solar PV demand.

- Low-cost financing for domestically manufactured equipment attached to policies to stimulate solar PV demand.

(This article is based on internal research and various National and International reports published by industry bodies, associations and organisations working for the solar and renewable energy industry)